If you invest in DAOs, you have to be an activist

There’s a saying about arguing with engineers that likens it to wrestling with pigs in the mud—after a while, you realize that the pig likes it. Activism defense mandates in investment banking are the cynical mud-wrestling pleasure of mimicking a potential activist assault. Sending clients pages and pages explaining what a crap job they’ve been doing and how they should all be hung, drawn and quartered is cheeky fun to an engineer (pig?) like me.

The driver behind a lot of investor activism is the idea that companies are undervalued relative to their potential because management interests fall out of alignment with shareholder interests.

The plan is that taking a more active role in governance can reset this alignment and over time the company value can return to its potential. Activist investors spend their time fixing situations where management and shareholder incentives have diverged the most. The potential for a financial return is in buying an underperforming company and spending time/resources agitating for change.

An intriguing recent example of value-based activism is when investors agitate for change on moral principles rather than purely financial grounds. Carl Icahn taking McDonald’s to task for repeated failures to improve animal welfare in its supply chain is a salient example. You could make the argument that there is also a financial motivation, in that as long as consumers increasingly demand better treatment of animals, companies are ill-serving shareholder interests by behaving unethically towards animals.

The art of defending against activism attacks is a combination of subtle expropriations of shareholder rights on a malicious side of the spectrum, and owning up to shortcomings on the other. The mere threat of an activist assault is a healthy market mechanism that helps keep observant managers on their toes.

The age of DAOs and governance tokens presents investors with a new dilemma around the degree of activism they should be willing to take. Protocol tokens are racing ahead of regulation to operate non-entities managed by non-employees. Legislators may well never catch up. How do you impose working regulations for employees who are geographically mobile and working for a set of immutable smart contracts on a blockchain? Another area of difference relative to modern corporations is that tokens make no formal or legal obligations of their non-employees to increase the monetary value of the tokens.

DAOs depend strongly on governance voting to guide their choices. This is also unlike most traditional organizations and will therefore demand different forms of investor engagement. Even cooperatives allow for delegated authority to the managers when it comes to day-to-day decisions or contract negotiations with third-parties. But DAOs need their token holders to run the day-to-day. Unfortunately, commitment tends to be quite low in the best instances.

Similar effects happen in highly decentralized countries. Switzerland, for example, regularly calls votes on local and national referendums on topics that range from power grid strategy to building height regulation. However, participation regularly struggles to crack 40%. Clearly, this is suboptimal to the functioning of a country. A majority of 40% of an electorate which itself is a subset of the total population of a country means that approving a referendum choice, far from being decentralized to the individual, is, in fact, quite concentrated in small, engaged constituencies.

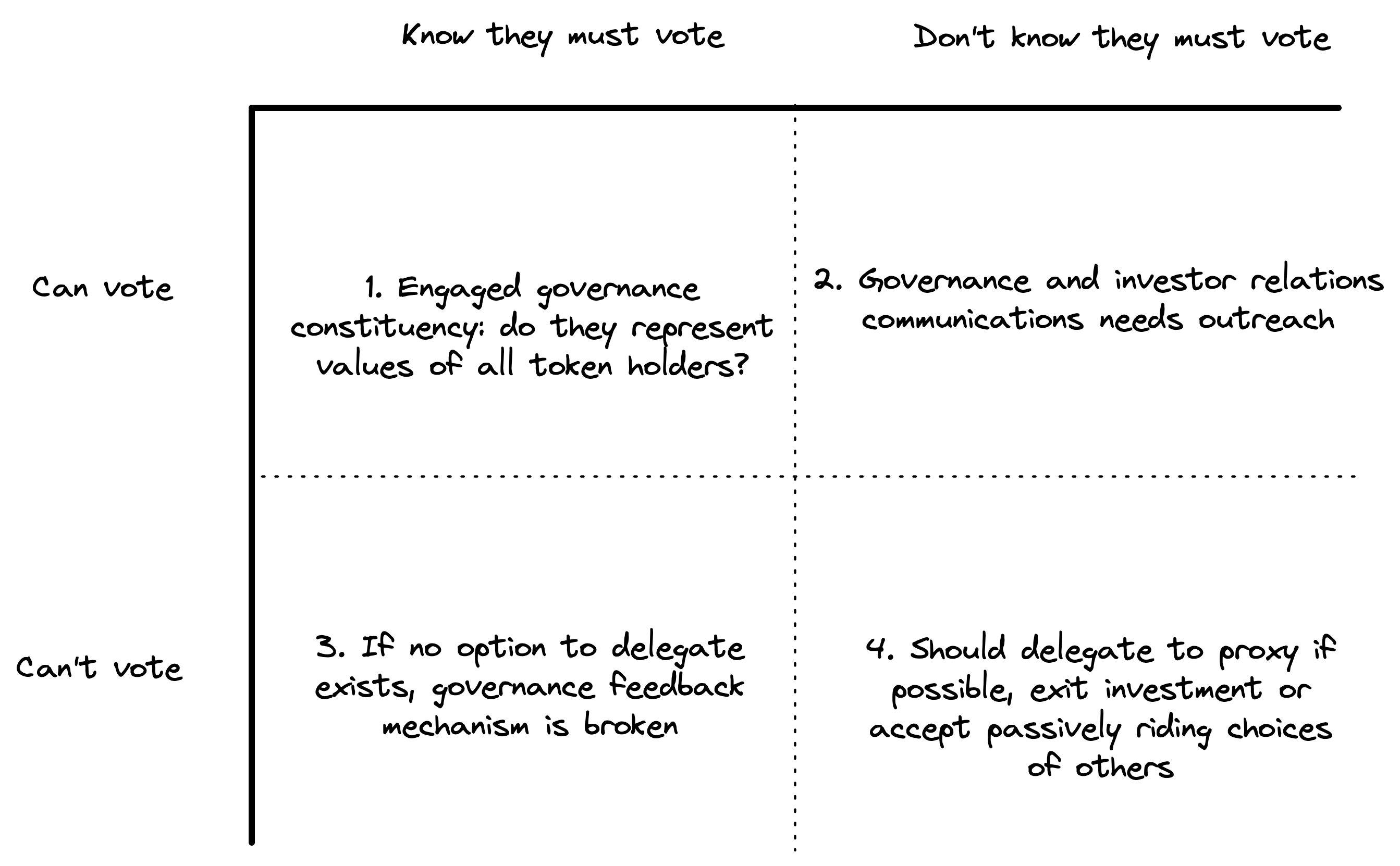

There may be multiple reasons behind disengagement in DAO governance, e.g.:

An engaged voting constituency may be aware of the responsibilities of voting in a DAO. Their experience with the protocol should be nurtured and kept. However, in situations of low commitment they may give the impression of monolithic voting blocks that are impossible to displace and disengage governance further.

Token holders with the power/ability and potentially time to engage with governance are the biggest easy-win for governance communications teams or investor relations. They may simply not appreciate the importance of their voting power. If a voter is small, they may feel it is useless. If the voter is large/institutional, they may feel it could be perceived as interfering with a public good. In either case, DAOs should prioritize efforts to reach them and ask for their engagement. Small token holders can still exercise aggregated power. Large token holders should use the tools of governance to cater to their long-term interest, tied as it is with the long-term interest of the protocol.

The most painful constituency to address for DAOs are token holders who are aware of the importance of their vote, regardless of their size, but are unable to. It may be as simple a barrier as technical infrastructure that is costly (costs gas) to use, in which case, moving to delegation systems or gasless voting is ideal.

Constituencies who are unaware of their importance as token holders and who do not have the ability to vote have both an infrastructure and an education barrier to cross. Perhaps they are small holders or hold their tokens on a centralized exchange. Governance should work to make delegation possible in centralized wallets or exchanges, for instance. It may well be the case that there is no particular investment thesis behind holding the token, in which case it begs the question of why stay invested at all? Ultimately, should the token holder wish to remain, they must get comfortable with their inability to affect outcomes and accept the result of other people’s decisions with the future of their token holdings.

Investing in a DAO is more akin to becoming a citizen of a country rather than a tourist or transient resident. Any value creation thesis that involves a DAO necessarily needs to involve governing actively to formulate the path to success.

DAO value creation must come from active governance given the rules of engagement. DAOs without an engaged base are a suboptimal equilibrium that results in organizational underperformance, unrepeatable outperformance or simply stasis in a stage of immature product adoption or development. Just being invested in a DAO commits the investor to taking an active role in the decisions that shape the outcomes. Work is delegated to contributors, but responsibility is shared with the token holders.

Investing in a DAO faces the asymmetric, non-linear return profile of early-stage venture-capital. The potential is huge as the protocols, being decentralized, can reach profitability faster than traditional high-growth startups if managed correctly, given that operating expenses can be atomized and shared among users of the blockchain. However, the road to achieving that goal is paved with commitments in time and resources for engagement, more akin to an operationally active private-equity investor in a mature-stage company.

Therefore, investors, both large and small, should take the wheel of their ownership and commit resources either to delegate their votes or participate. This is a profitable trade provided the undervaluation or immaturity of a protocol relative to its potential is large enough to offset ongoing management expenses of dedicating a resource to comb through the forums and spend 2-3 hours a day on Discord.

If you invest in a DAO, you have to be an activist.